News

Denison Mines Corp. Reports Highlights of 2015 Results

TORONTO, ONTARIO--(Marketwired - March 9, 2016) - Denison Mines Corp. ("Denison" or the "Company") (TSX:DML)(NYSE MKT:DNN) today filed its Consolidated Financial Statements and Management's Discussion & Analysis ("MD&A") for the financial year ended December 31, 2015. Both documents can be found on the Company's website at www.denisonmines.com or on SEDAR (at www.sedar.com) and EDGAR (at www.sec.gov/edgar.shtml). The highlights provided below are derived from these documents and should be read in conjunction with them. All amounts in this release are in U.S. dollars unless otherwise stated.

David Cates, President and CEO of Denison commented "In 2015, Denison achieved a key milestone with the completion of a maiden resource estimate for our Gryphon deposit on the Wheeler River property - which was already host to the exceptionally high-grade Phoenix deposit. The addition of the Gryphon deposit represents a significant increase in the estimated mineral resources at Denison's 60% owned Wheeler River property, and establishes the project as one of the largest and highest grade undeveloped uranium projects in the Athabasca Basin region."

2015 HIGHLIGHTS

- Reported a significant increase in estimated mineral resources at the Wheeler River property

The Company completed an initial mineral resource estimate for the basement hosted Gryphon uranium deposit, which is located three kilometres to the northwest of the high-grade unconformity hosted Phoenix deposit. The Gryphon deposit is estimated to contain an inferred mineral resource of 43.0 million pounds U3O8 at an average grade of 2.3% U3O8. Together with the high-grade Phoenix deposit, Wheeler River is now estimated to contain indicated mineral resources of 70.2 million pounds U3O8 at an average grade of 19.1% U3O8 and inferred mineral resources totaling 44.1 million pounds U3O8 at a combined grade of 2.34% U3O8 (see Denison news release dated November 3, 2015).

- Moving ahead at the Wheeler River Property

A Preliminary Economic Analysis ("PEA") was initiated in 2015 to evaluate the economic merit of the co-development of the Gryphon and Phoenix deposits and is expected to be completed in the first half of 2016. Subject to a positive outcome from the PEA, the Company plans to initiate work on a Prefeasibility Study and environmental assessment work as part of a 2016 evaluation budget of CAD$2,600,000 (CAD$1,600,000 Denison's share).

- Experienced continued exploration success at the Wheeler River property

Exploration drilling results for the area in the vicinity of the Gryphon deposit continued to highlight the mineralization potential of this area. During 2015, a total of 16 drill holes were completed up plunge and along the sub-Athabasca unconformity to the southwest of the Gryphon deposit along the K-North trend. The drilling successfully identified approximately 2.3 kilometres of mineralized strike. The mineralization occurs both at the unconformity and immediately below within the basement, indicating further potential along the unconformity to the southwest and within the basement below. The best result to date occurs at the unconformity, 800 metres to the south of Gryphon, with drill hole WR-597 intersecting 4.5% U3O8 over 4.5 metres (see Denison news release dated June 4, 2015). In February 2016 Denison reported a new intersection of high-grade uranium within the basement roughly 100 metres to the north of the Gryphon deposit, (see Denison news release dated February 9, 2016).

- Generated positive 2015 exploration results at other exploration pipeline properties in the infrastructure rich eastern Athabasca Basin

At the 68.85% owned Murphy Lake property, Denison intersected a new zone of uranium mineralization, highlighted by drill hole MP-15-03, which returned a mineralized interval of 0.25% U3O8 over 6.0 metres at the sub-Athabasca unconformity (see Denison news release dated July 29, 2015). At the 61.55% owned Waterbury Lake property, the Company intersected weak uranium mineralization and strong alteration and/or structure at the Oban target area. At the 100% owned Crawford Lake property, the Company extended a large zone of significant sandstone alteration along the CR-2 and CR-5 conductors, which is now confirmed over a strike length of 2.9 kilometres.

- Exceeded initial 2015 guidance for toll milling revenue at McClean Lake

The McClean Lake mill, in which Denison owns a 22.5% interest, packaged approximately 11.3 million pounds U3O8 during the year (initially targeted at six to eight million packaged pounds) for the Cigar Lake Joint Venture ("CLJV"), generating toll milling revenues for Denison of $3.2 million.

- Completed the sale of the Company's Mongolian interests for consideration of up to $13.25 million

Denison received $1.25 million in initial payments on the closing of the sale of its Mongolian interests. Denison has the rights to receive additional proceeds of up to $12 million, conditional on achieving certain milestones associated with the Mongolian projects.

ABOUT DENISON

Denison is a uranium exploration and development company with interests focused in the Athabasca Basin region of northern Saskatchewan, Canada. In addition to its 60% owned Wheeler River project, which hosts the high grade Phoenix and Gryphon uranium deposits, Denison's exploration portfolio consists of numerous projects covering over 390,000 hectares in the eastern Athabasca Basin. Denison's interests in Saskatchewan also include a 22.5% ownership interest in the McClean Lake joint venture ("MLJV"), which includes several uranium deposits and the McClean Lake uranium mill, plus a 25.17% interest in the Midwest deposit and a 61.55% interest in the J Zone deposit on the Waterbury Lake property. Both the Midwest and J Zone deposits are located within 20 kilometres of the McClean Lake mill. Internationally, Denison owns 100% of the Mutanga uranium project in Zambia, 100% of the uranium-silver-copper Falea project in Mali and a 90% interest in the Dome uranium project in Namibia.

Denison is engaged in mine decommissioning and environmental services through its Denison Environmental Services ("DES").

Denison is also the manager of Uranium Participation Corporation ("UPC"), a publicly traded company listed on the TSX under the symbol "U", which invests in uranium oxide in concentrates ("U3O8") and uranium hexafluoride.

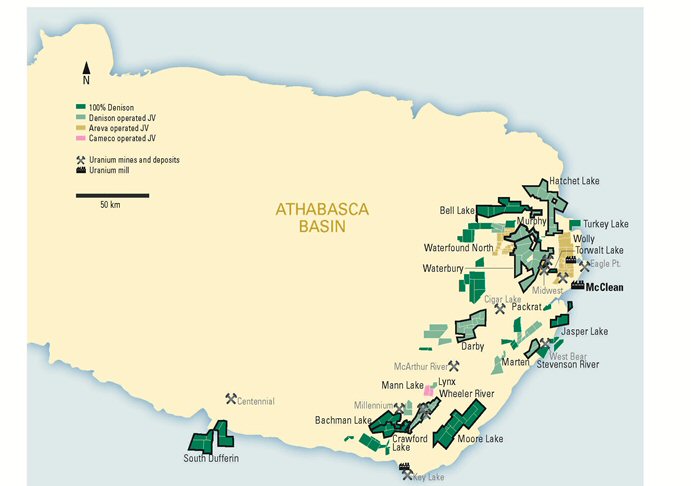

EASTERN ATHABASCA LAND POSITION

The Company's land position in the infrastructure rich eastern Athabasca Basin, as of December 31, 2015, is illustrated below. Denison's active exploration properties are outlined in bold.

To view the map associated with this release, please visit the following link: http://media3.marketwire.com/docs/dml0309map.jpg.

SELECTED ANNUAL FINANCIAL INFORMATION

| (in thousands, except for per share amounts) | Year Ended December 31, 2015 |

Year Ended December 31, 2014 |

||||

| Results of Continuing Operations: | ||||||

| Total revenues | $ | 12,670 | $ | 9,619 | ||

| Mineral property exploration | $ | (14,257 | ) | $ | (14,401 | ) |

| Impairment of mineral properties | $ | (27,767 | ) | $ | (1,745 | ) |

| Net loss | $ | (61,737 | ) | $ | (28,266 | ) |

| Basic and diluted loss per share | $ | (0.12 | ) | $ | (0.06 | ) |

| Results from Mongolian Discontinued Operations: | ||||||

| Net income (loss) | $ | 10,177 | $ | (3,437 | ) | |

| Basic and diluted income per share | $ | 0.02 | $ | (0.01 | ) | |

(in thousands) |

As at December 31, 2015 |

As at December 31, 2014 |

||

| Financial Position: | ||||

| Cash and cash equivalents | $ | 5,367 | $ | 18,640 |

| Short term investments | 7,282 | 4,381 | ||

| Long term investments | 496 | 954 | ||

| Cash, cash equivalents and investments | $ | 13,145 | $ | 23,975 |

| Working capital | $ | 12,772 | $ | 22,542 |

| Property, plant and equipment | $ | 188,250 | $ | 270,388 |

| Total assets | $ | 212,758 | $ | 311,330 |

| Total long-term liabilities | $ | 38,125 | $ | 42,291 |

RESULTS OF OPERATIONS

Revenues

The McClean Lake mill continued to process ore received from the Cigar Lake mine. The mill packaged approximately 11.3 million pounds U3O8 for the CLJV. The Company's share of toll milling revenue during 2015 totaled $3,155,000.

Revenue from Denison Environmental Services ("DES") during 2015 was $7,607,000, improving on 2014 due to increased activity at certain care and maintenance sites.

Revenue from the Company's management contract with UPC was $1,822,000 during 2015.

Operating expenses

Canadian mining segment operating expenses include depreciation, development and standby costs, as well as certain adjustments to the estimates of future reclamation liabilities at McClean Lake, Midwest and Elliot Lake. Operating expenses in 2015 were $4,554,000, including depreciation of the McClean Lake mill of $1,627,000.

DES operating expenses during 2015 totaled $6,875,000, related primarily to the construction and consulting services provided to clients and includes labour and other costs.

General and administrative expenses

Total general and administrative expenses were $6,463,000 during 2015. These costs are mainly comprised of head office salaries and benefits, office costs in multiple regions, audit and regulatory costs, legal fees, investor relations expenses, project costs and all other costs related to operating a public company with listings in Canada and the United States. Also included was $1,461,000 related to the failed transaction with Fission Uranium Corp.

Impairment - Mineral Properties

During 2015, the Company recognized a non-cash impairment of $25,164,000 against the value of its African mining segment, which included significant carrying values for the Falea, Mutanga and Dome projects, and also recognized non-cash impairment charges of $2,603,000, to fully impair the carrying value of three of its non-core Canadian exploration properties.

Foreign exchange income and expense

During 2015, a foreign exchange loss of $16.0 million was recognized due to unfavourable fluctuations in foreign exchange rates impacting the revaluation of intercompany debt for the Company's African related operations.

Mongolian Discontinued Operations

Income from discontinued operations was $10,177,000, which mainly comprised of the gain on disposal of $8,374,000 and transactional foreign exchange income of $2,873,000, partly offset by exploration, operating and administrative expenses of $1,091,000. The gain on the disposal consisted of $1,250,000 in cash consideration, less transaction costs of $337,000, a favourable cumulative translation adjustment of $13,680,000, offset by the carrying value of the net assets of $6,219,000. Denison is entitled to up to $12,000,000 in additional proceeds that are contingent on the approval of certain mining licenses and other milestones.

LIQUIDITY AND CAPITAL RESOURCES

Cash, cash equivalents, GICs and other investments were $13,145,000 at December 31, 2015. The Company holds a large majority of its cash, cash equivalents, and investments in Canadian dollars. As at December 31, 2015, the Company's cash, cash equivalents and current investments amount to CAD$17.5 million. The Company's CAD$24 million credit facility available for non-financial letters of credit was extended in January 2016 to January 2017. The facility contains a covenant that requires the Company to maintain a minimum cash balance of CAD$5 million on deposit with the Bank of Nova Scotia.

OUTLOOK FOR 2016

In 2016, the Company will focus on increasing its mineral resource base in the Athabasca Basin and advancing the Wheeler River project. The 2016 winter exploration program commenced in January with a focus on the Company's Wheeler River project and other high priority properties located in the infrastructure rich eastern Athabasca Basin.

| (in thousands) | 2016 BUDGET (1) | ||

| Canada | |||

| Toll Milling Revenue & Mineral Sales | $ | 5,450 | |

| Development & Operations | (2,450 | ) | |

| Mineral Property Exploration & Evaluation | (13,000 | ) | |

| (10,000 | ) | ||

| Africa | |||

| Zambia, Mali and Namibia | (1,290 | ) | |

| (1,290 | ) | ||

| Other | |||

| UPC Management Services | 1,520 | ||

| DES Environmental Services | 920 | ||

| Corporate Administration & Other | (4,200 | ) | |

| (1,760 | ) | ||

| Total | $ | (13,050 | ) |

| (1) | Budget figures have been converted using a US$ to CAD$ exchange rate of 1.30. |

CANADA

Toll Milling Revenue & Mineral Sales

Provided regulatory approvals are secured to increase the annual license limit, the McClean Lake mill is expected to produce 16 million pounds U3O8 during 2016. Denison's share of revenue from toll milling of the Cigar Lake ore and the sale of approximately 25,000 pounds U3O8, currently held by Denison in inventory, is budgeted to be $5.4 million (CAD$7.1 million).

Development & Operations

In 2016, Denison's share of operating and capital expenditures at McClean Lake and Midwest are budgeted to be $1.6 million (CAD$2.1 million). Operating expenditures include $797,000 (CAD$1.04 million) in respect of Denison's share of the planned 2016 budget for the Surface Access Borehole Resource Extraction ("SABRE") program.

Reclamation expenditures at Elliot Lake are budgeted to be $665,000 (CAD$864,000).

Mineral Property Exploration & Evaluation

Denison expects to operate and/or participate in a total of 15 exploration programs (including 13 drilling programs totaling approximately 75,000 metres), of which Wheeler River will continue to be the primary focus. The total budget for all of these programs, inclusive of the evaluation work planned for Wheeler River, is budgeted to be CAD$24.6 million (Denison's share, CAD$16.9 million).

Wheeler River - Exploration

A total of 47,000 metres of exploration drilling is planned at Wheeler River between the winter and summer drill programs, along with geophysical surveys at a total cost of CAD$10.0 million (Denison's share, CAD$6.0 million).

Exploration drilling planned for 2016 will continue to test the unconformity to the southwest of Gryphon as well as numerous basement targets near Gryphon.

Wheeler River - Evaluation

The PEA is expected to be completed during the first half of 2016. Subject to a positive outcome from the PEA, the Company plans to initiate work on a Prefeasibility Study and environmental assessment work with an approximate budget for 2016 of CAD$2.6 million (Denison's share, CAD$1.6 million).

Other High Priority Exploration Properties

Drilling at the Company's high priority exploration properties is planned to continue at Murphy Lake, Crawford Lake and Waterbury Lake during 2016. Drill programs are also planned for Denison's non-operated joint venture projects, including Mann Lake, Wolly and McClean Lake.

Environmental services

Revenue from operations at DES during 2016 is budgeted to be $7.2 million (CAD$9.4 million) and operating and overhead expenses are budgeted to be $6.1 million (CAD$7.9 million). Capital expenditures at DES are budgeted to be $230,000 (CAD$300,000).

Corporate administration and other

Budgeted at $3.85 million (CAD$5.0 million) in 2016, corporate administration costs include all head office salaries and benefits, office costs, audit and regulatory costs, legal fees, investor relations expenses and all other costs related to operating a public company with listings in Canada and the United States.

Net management fees earned during 2016 from UPC are budgeted at $1.5 million (CAD$1.95 million).

Letter of credit and standby fees relating to the 2016 Credit Facility are budgeted to be $400,000 (CAD$520,000).

TECHNICAL INFORMATION

Further details regarding the Gryphon deposit and the current mineral resources estimated at Wheeler River are provided in the report titled "Technical Report on a Mineral Resource Estimate For The Wheeler River Property, Eastern Athabasca Basin, Northern Saskatchewan, Canada.", dated Nov. 25, 2015, authored by William E. Roscoe Ph.D, P.Eng. and Mark B. Mathisen C.P.G of RPA Inc. A copy of this report is available under Denison's profile on SEDAR (www.sedar.com).

The disclosure of a scientific or technical nature contained in this news release was prepared by Dale Verran, MSc, Pr.Sci.Nat., Denison's Vice President, Exploration, who is a Qualified Person in accordance with the requirements of NI 3-101. For a description of the quality assurance program and quality control measures applied by Denison, please see Denison's Annual Information Form dated March 5, 2015 filed under the Company's profile on SEDAR at www.sedar.com.

Cautionary Statement Regarding Forward-Looking Statements

Certain information contained in this press release constitutes "forward-looking information", within the meaning of the United States Private Securities Litigation Reform Act of 1995 and similar Canadian legislation concerning the business, operations and financial performance and condition of Denison.

Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as "plans", "expects", "budget", "scheduled", "estimates", "forecasts", "intends", "anticipates", or "believes", or the negatives and/or variations of such words and phrases, or state that certain actions, events or results "may", "could", "would", "might" or "will be taken", "occur", "be achieved" or "has the potential to".

In particular, this press release contains forward-looking information pertaining to the following: the likelihood of completing and benefits to be derived from corporate transactions, including the potential for receipt of any contingent payments; the estimates of Denison's mineral reserves and mineral resources; completion of the PEA; expectations regarding the toll milling of Cigar Lake ores; expectations regarding revenues and expenditure from operations at DES; capital expenditure programs, estimated exploration and development expenditures and reclamation costs and Denison's share of same; exploration, development and expansion plans and objectives; and statements regarding anticipated budgets, fees and expenditures. Statements relating to "mineral reserves" or "mineral resources" are deemed to be forward-looking information, as they involve the implied assessment, based on certain estimates and assumptions that the mineral reserves and mineral resources described can be profitably produced in the future.

Forward looking statements are based on the opinions and estimates of management as of the date such statements are made, and they are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of Denison to be materially different from those expressed or implied by such forward-looking statements. Denison believes that the expectations reflected in this forward-looking information are reasonable but no assurance can be given that these expectations will prove to be accurate and may differ materially from those anticipated in this forward looking information. For a discussion in respect of risks and other factors that could influence forward-looking events, please refer to the factors discussed in the MD&A under the heading "Risk Factors". These factors are not, and should not be construed as being exhaustive.

Accordingly, readers should not place undue reliance on forward-looking statements. The forward-looking information contained in this press release is expressly qualified by this cautionary statement. Any forward-looking information and the assumptions made with respect thereto speaks only as of the date of this press release. Denison does not undertake any obligation to publicly update or revise any forward-looking information after the date of this press release to conform such information to actual results or to changes in Denison's expectations except as otherwise required by applicable legislation.

Cautionary Note to United States Investors Concerning Estimates of Measured, Indicated and Inferred Mineral Resources: This press release may use the terms "measured", "indicated" and "inferred" mineral resources. United States investors are advised that while such terms are recognized and required by Canadian regulations, the United States Securities and Exchange Commission does not recognize them. "Inferred mineral resources" have a great amount of uncertainty as to their existence, and as to their economic and legal feasibility. It cannot be assumed that all or any part of an inferred mineral resource will ever be upgraded to a higher category. Under Canadian rules, estimates of inferred mineral resources may not form the basis of feasibility or other economic studies. United States investors are cautioned not to assume that all or any part of measured or indicated mineral resources will ever be converted into mineral reserves. United States investors are also cautioned not to assume that all or any part of an inferred mineral resource exists, or is economically or legally mineable.

David Cates

President and Chief Executive Officer

(416) 979-1991 ext 362

Denison Mines Corp.

Sophia Shane

Investor Relations

(604) 689-7842

www.denisonmines.com

{kind=link}